ML Data Construction Showcase¶

Revenue Forecasting From Multi-Source Data (Synthetic E-commerce Example)¶

Learning objectives¶

Build a realistic ML-ready dataset from master data + event logs.

Construct a target label from business logic: future 90-day revenue.

Engineer behavioral features from historical transactions.

Encode categorical variables with one-hot encoding.

Prevent temporal leakage via strict observation vs prediction windows.

Business framing¶

For each customer at reference date t, predict revenue in the next 90 days. This mirrors production ML settings where we only have historical data at prediction time, while labels come from future outcomes.

[1]:

import numpy as np

import pandas as pd

from datetime import timedelta

from sklearn.compose import ColumnTransformer

from sklearn.preprocessing import OneHotEncoder

[2]:

# Set the random seed for reproducibility

SEED = 42

# Create a random number generator with the specified seed

rng = np.random.default_rng(SEED)

np.random.seed(SEED)

print(f"Random seed set to {SEED}")

Random seed set to 42

SECTION B — Generate Synthetic Raw Data¶

SECTION B.1 — Generate Synthetic Customer Master Table¶

[3]:

# Synthetic customer master table

n_customers = 1200

# Define the range of customer IDs

customer_ids = [f"C{i:04d}" for i in range(1, n_customers + 1)]

# Define the values for the categorical features

countries = ["DE", "FR", "CH", "IT", "ES"]

segments = ["Budget", "Standard", "Premium"]

channels = ["Organic", "Paid Ads", "Referral", "Affiliate"]

# Use a fixed synthetic timeline so notebook behavior is deterministic

synthetic_today = pd.Timestamp("2025-01-31")

signup_start = synthetic_today - pd.Timedelta(days=730) # last 24 months

# Generate random signup dates for each customer

signup_offsets = rng.integers(0, 731, size=n_customers)

signup_dates = signup_start + pd.to_timedelta(signup_offsets, unit="D")

# Create a DataFrame with the generated data

customers = pd.DataFrame(

{

"customer_id": customer_ids,

"signup_date": pd.to_datetime(signup_dates),

"country": rng.choice(countries, size=n_customers, p=[0.25, 0.2, 0.15, 0.2, 0.2]),

"customer_segment": rng.choice(segments, size=n_customers, p=[0.4, 0.45, 0.15]),

"acquisition_channel": rng.choice(channels, size=n_customers, p=[0.35, 0.3, 0.2, 0.15]),

}

)

customers.head()

[3]:

| customer_id | signup_date | country | customer_segment | acquisition_channel | |

|---|---|---|---|---|---|

| 0 | C0001 | 2023-04-07 | CH | Standard | Referral |

| 1 | C0002 | 2024-08-19 | IT | Standard | Paid Ads |

| 2 | C0003 | 2024-05-24 | ES | Budget | Organic |

| 3 | C0004 | 2023-12-18 | IT | Standard | Referral |

| 4 | C0005 | 2023-12-14 | ES | Standard | Organic |

Section B.2. Generate synthetic transaction event table¶

[4]:

# Synthetic transaction event table

# Design choices as underlying assumptions & distributional choices:

# - Premium customers spend more

# - Paid Ads customers tend to churn more / have fewer repeat purchases

# - Some customers have no transactions

# - Mild recency + seasonality effects

transaction_rows = []

# Define the range of transaction dates

tx_global_start = synthetic_today - pd.Timedelta(days=420) # >12 months history

tx_global_end = synthetic_today + pd.Timedelta(days=120) # includes future wrt reference date

# Define the multipliers for the segment frequency and amount

segment_freq_mult = {"Budget": 0.8, "Standard": 1.0, "Premium": 1.35}

segment_amount_mult = {"Budget": 0.75, "Standard": 1.0, "Premium": 1.8}

channel_freq_mult = {"Organic": 1.1, "Paid Ads": 0.75, "Referral": 1.05, "Affiliate": 0.9}

channel_no_tx_bonus = {"Organic": 0.00, "Paid Ads": 0.12, "Referral": 0.00, "Affiliate": 0.03}

# Iterate over each customer in the customers DataFrame

for row in customers.itertuples(index=False):

cid = row.customer_id

signup = row.signup_date

seg = row.customer_segment

ch = row.acquisition_channel

# Customers with short tenure have fewer possible transactions

tenure_days = max((synthetic_today - signup).days, 1)

tenure_factor = min(tenure_days / 365.0, 1.4)

# Calculate the base lambda for the Poisson distribution

base_lambda = 4.5 * segment_freq_mult[seg] * channel_freq_mult[ch] * tenure_factor

# Probability of no transactions at all

p_no_tx = 0.08 + channel_no_tx_bonus[ch]

if rng.random() < p_no_tx:

continue

# Generate the number of transactions for the customer following a Poisson distribution with the base lambda

n_tx = rng.poisson(base_lambda)

if n_tx <= 0:

n_tx = 1

# Mild recency effect: some users get extra recent transactions

if rng.random() < 0.25:

n_tx += rng.integers(1, 4)

# Define the range of transaction dates

tx_start = max(tx_global_start, signup)

tx_end = tx_global_end

n_days = max((tx_end - tx_start).days, 1)

# Build date weights: slightly more recent + mild seasonal bump in Nov/Dec

date_index = pd.date_range(tx_start, tx_end, freq="D")

recency_weight = np.linspace(0.8, 1.2, len(date_index))

seasonal_weight = np.where(date_index.month.isin([11, 12]), 1.15, 1.0)

day_weights = recency_weight * seasonal_weight

day_weights = day_weights / day_weights.sum()

# Choose the transaction dates for the customer from the date_index array

chosen_dates = rng.choice(date_index, size=n_tx, replace=True, p=day_weights)

# Iterate over the chosen transaction dates

for tx_date in chosen_dates:

# Log-normal amount with segment effect + occasional outliers

amount = rng.lognormal(mean=3.6, sigma=0.55) * segment_amount_mult[seg]

# Occasionally generate outlier purchases

if rng.random() < 0.015:

amount *= rng.uniform(5, 12) # outlier purchases

# Small seasonal uplift around Nov/Dec

if pd.Timestamp(tx_date).month in [11, 12]:

amount *= 1.08

# Append the transaction data to the transaction_rows list

transaction_rows.append(

{

"customer_id": cid,

"transaction_date": pd.Timestamp(tx_date),

"amount": float(round(amount, 2)),

}

)

# Convert the transaction_rows list into a DataFrame

transactions = pd.DataFrame(transaction_rows)

# Sort the transactions by customer ID and transaction date

transactions = transactions.sort_values(["customer_id", "transaction_date"]).reset_index(drop=True)

# Display the first few rows of the transactions DataFrame

transactions.head()

[4]:

| customer_id | transaction_date | amount | |

|---|---|---|---|

| 0 | C0001 | 2024-02-18 | 30.96 |

| 1 | C0001 | 2024-04-14 | 24.45 |

| 2 | C0001 | 2024-07-15 | 44.53 |

| 3 | C0001 | 2024-09-05 | 34.86 |

| 4 | C0001 | 2024-11-07 | 23.09 |

[5]:

# Basic sanity checks

print("Customers head:")

display(customers.head())

# Display the first few rows of the transactions DataFrame

print("\nTransactions head:")

display(transactions.head())

# Print the row counts for the customers and transactions DataFrames

print("\nRow counts")

print("customers:", len(customers))

print("transactions:", len(transactions))

# Print the number of unique customers in the customers and transactions DataFrames

print("\nUnique customers")

print("customers table:", customers["customer_id"].nunique())

print("transactions table:", transactions["customer_id"].nunique())

# Calculate the number of customers with no transactions

customers_with_no_tx = customers.loc[~customers["customer_id"].isin(transactions["customer_id"]), "customer_id"].nunique()

print("customers with no transactions:", customers_with_no_tx)

# Print the number of missing values in the customers and transactions DataFrames

print("\nMissing values")

print("customers:\n", customers.isna().sum())

print("transactions:\n", transactions.isna().sum())

Customers head:

| customer_id | signup_date | country | customer_segment | acquisition_channel | |

|---|---|---|---|---|---|

| 0 | C0001 | 2023-04-07 | CH | Standard | Referral |

| 1 | C0002 | 2024-08-19 | IT | Standard | Paid Ads |

| 2 | C0003 | 2024-05-24 | ES | Budget | Organic |

| 3 | C0004 | 2023-12-18 | IT | Standard | Referral |

| 4 | C0005 | 2023-12-14 | ES | Standard | Organic |

Transactions head:

| customer_id | transaction_date | amount | |

|---|---|---|---|

| 0 | C0001 | 2024-02-18 | 30.96 |

| 1 | C0001 | 2024-04-14 | 24.45 |

| 2 | C0001 | 2024-07-15 | 44.53 |

| 3 | C0001 | 2024-09-05 | 34.86 |

| 4 | C0001 | 2024-11-07 | 23.09 |

Row counts

customers: 1200

transactions: 4636

Unique customers

customers table: 1200

transactions table: 1046

customers with no transactions: 154

Missing values

customers:

customer_id 0

signup_date 0

country 0

customer_segment 0

acquisition_channel 0

dtype: int64

transactions:

customer_id 0

transaction_date 0

amount 0

dtype: int64

[6]:

# Save the synthetic data to a CSV file

customers.to_csv("data/customers.csv", index=False)

transactions.to_csv("data/transactions.csv", index=False)

print("Synthetic data saved to CSV files")

Synthetic data saved to CSV files

SECTION C — Define Temporal Windows and Reference Date¶

Now, we have (synthesized) our raw data set. Often this is the starting point of data that you get from your business stakeholders.

Next, we must separate:

Observation window: historical data used to build features.

Prediction window: future period used to construct the label.

If we accidentally include prediction-window information in features, we create temporal leakage.

[7]:

# Reference date and windows

# Choose t so we still have enough future transactions to build labels

reference_date = transactions["transaction_date"].max() - pd.Timedelta(days=120)

# Define the observation and prediction windows in days, as discussed in the slides

observation_days = 180

prediction_days = 90

# Calculate the start and end dates for the observation and prediction windows

obs_start = reference_date - pd.Timedelta(days=observation_days)

obs_end = reference_date

# Calculate the start and end dates for the prediction window

pred_start = reference_date

pred_end = reference_date + pd.Timedelta(days=prediction_days)

# Print the reference date and the observation and prediction windows

print("reference_date (t):", reference_date.date())

print(f"observation window: [{obs_start.date()}, {obs_end.date()}]")

print(f"prediction window: ({pred_start.date()}, {pred_end.date()}]")

reference_date (t): 2025-01-31

observation window: [2024-08-04, 2025-01-31]

prediction window: (2025-01-31, 2025-05-01]

SECTION D — Label Construction (Future Revenue)¶

Define target for customer i as:

[ y_i = \sum `:nbsphinx-math:text{amount}`_{i, d} \text{ for } d :nbsphinx-math:`in `(t, t+90] ]

Customers with no transactions in the prediction window get label 0.

[8]:

# Prediction-window transactions: (t, t+90]

pred_tx = transactions[

(transactions["transaction_date"] > pred_start)

& (transactions["transaction_date"] <= pred_end)

].copy()

# Group the transactions by customer ID and sum the amount for each customer

label_df = (

pred_tx.groupby("customer_id", as_index=False)["amount"]

.sum()

.rename(columns={"amount": "future_revenue_90d"})

)

# Ensure every customer exists in label table

label_df = customers[["customer_id"]].merge(label_df, on="customer_id", how="left")

label_df["future_revenue_90d"] = label_df["future_revenue_90d"].fillna(0.0)

# Print a summary of the label distribution

print("Label summary:")

print(label_df["future_revenue_90d"].describe())

# Calculate the percentage of zero labels

pct_zero = (label_df["future_revenue_90d"] == 0).mean() * 100

print(f"Percent zero labels: {pct_zero:.2f}%")

Label summary:

count 1200.000000

mean 46.428433

std 80.516101

min 0.000000

25% 0.000000

50% 19.955000

75% 62.417500

max 1070.010000

Name: future_revenue_90d, dtype: float64

Percent zero labels: 45.17%

SECTION E — Feature Engineering From Observation Window (Past Behavior)¶

We engineer RFM-style and trend features only from historical data in [t-180, t].

No transaction after t is used for features (prevents leakage).

SECTION E.1: Define the range of the past 180 days¶

[9]:

# Observation-window transactions: [t-180, t], i.e. 180 days before t

obs_tx = transactions[

(transactions["transaction_date"] >= obs_start)

& (transactions["transaction_date"] <= obs_end)

].copy()

obs_tx["tx_day"] = obs_tx["transaction_date"].dt.normalize()

obs_tx.head()

[9]:

| customer_id | transaction_date | amount | tx_day | |

|---|---|---|---|---|

| 3 | C0001 | 2024-09-05 | 34.86 | 2024-09-05 |

| 4 | C0001 | 2024-11-07 | 23.09 | 2024-11-07 |

| 5 | C0001 | 2025-01-06 | 54.76 | 2025-01-06 |

| 13 | C0004 | 2024-09-20 | 27.63 | 2024-09-20 |

| 14 | C0004 | 2024-10-24 | 20.84 | 2024-10-24 |

SECTION E.2. Core Behavior Features¶

[10]:

# Core behavior features in observation window

# Group by customer ID and calculate the following metrics:

# - last_purchase_date: the latest transaction date for each customer

# - frequency: the number of transactions for each customer

# - monetary_total: the total amount spent by each customer

# - active_days: the number of unique days on which each customer has made a purchase

obs_agg = obs_tx.groupby("customer_id").agg(

last_purchase_date=("transaction_date", "max"),

frequency=("amount", "count"),

monetary_total=("amount", "sum"),

active_days=("tx_day", "nunique"),

)

# Calculate the average order value for each customer

obs_agg["avg_order_value"] = obs_agg["monetary_total"] / obs_agg["frequency"]

obs_agg = obs_agg.reset_index()

# Recency (days since last purchase)

obs_agg["recency_days"] = (reference_date - obs_agg["last_purchase_date"]).dt.days

obs_agg.head()

[10]:

| customer_id | last_purchase_date | frequency | monetary_total | active_days | avg_order_value | recency_days | |

|---|---|---|---|---|---|---|---|

| 0 | C0001 | 2025-01-06 | 3 | 112.71 | 3 | 37.570 | 25 |

| 1 | C0004 | 2024-10-24 | 2 | 48.47 | 2 | 24.235 | 99 |

| 2 | C0005 | 2024-12-01 | 1 | 49.24 | 1 | 49.240 | 61 |

| 3 | C0008 | 2024-12-16 | 2 | 80.94 | 2 | 40.470 | 46 |

| 4 | C0009 | 2024-12-01 | 2 | 171.99 | 2 | 85.995 | 61 |

SECTION E.3. Trend features¶

[11]:

# Calculate the sum of the amount for each customer in the recent 30 days

recent_30d = obs_tx[

(obs_tx["transaction_date"] > (reference_date - pd.Timedelta(days=30)))

& (obs_tx["transaction_date"] <= reference_date)

]

# Calculate the sum of the amount for each customer in the previous 30 days

prev_30d = obs_tx[

(obs_tx["transaction_date"] > (reference_date - pd.Timedelta(days=60)))

& (obs_tx["transaction_date"] <= (reference_date - pd.Timedelta(days=30)))

]

# Calculate the sum of the amount for each customer in the recent 30 days

recent_30d_spend = (

recent_30d.groupby("customer_id", as_index=False)["amount"]

.sum()

.rename(columns={"amount": "recent_30d_spend"})

)

# Calculate the sum of the amount for each customer in the previous 30 days

prev_30d_spend = (

prev_30d.groupby("customer_id", as_index=False)["amount"]

.sum()

.rename(columns={"amount": "prev_30d_spend"})

)

# Merge the recent 30 days spend and previous 30 days spend into the observation aggregate DataFrame

features_df = obs_agg.merge(recent_30d_spend, on="customer_id", how="left")

features_df = features_df.merge(prev_30d_spend, on="customer_id", how="left")

features_df[["recent_30d_spend", "prev_30d_spend"]] = features_df[["recent_30d_spend", "prev_30d_spend"]].fillna(0.0)

features_df["spend_trend"] = features_df["recent_30d_spend"] - features_df["prev_30d_spend"]

features_df.head()

[11]:

| customer_id | last_purchase_date | frequency | monetary_total | active_days | avg_order_value | recency_days | recent_30d_spend | prev_30d_spend | spend_trend | |

|---|---|---|---|---|---|---|---|---|---|---|

| 0 | C0001 | 2025-01-06 | 3 | 112.71 | 3 | 37.570 | 25 | 54.76 | 0.00 | 54.76 |

| 1 | C0004 | 2024-10-24 | 2 | 48.47 | 2 | 24.235 | 99 | 0.00 | 0.00 | 0.00 |

| 2 | C0005 | 2024-12-01 | 1 | 49.24 | 1 | 49.240 | 61 | 0.00 | 0.00 | 0.00 |

| 3 | C0008 | 2024-12-16 | 2 | 80.94 | 2 | 40.470 | 46 | 0.00 | 34.31 | -34.31 |

| 4 | C0009 | 2024-12-01 | 2 | 171.99 | 2 | 85.995 | 61 | 0.00 | 0.00 | 0.00 |

Data Cleansing!!¶

Missing-value handling choices:

Customers with no observation-window transactions get

frequency=0,monetary_total=0,active_days=0,recent_30d_spend=0,prev_30d_spend=0,spend_trend=0.avg_order_valueis set to 0 whenfrequency=0.recency_daysis set to a large value (observation_days + 1) for „not recently active“ customers.

[12]:

# Merge engineered features into customer table

model_base = customers.merge(features_df, on="customer_id", how="left")

# Fill missing values with 0.0 for the following columns

fill_zero_cols = [

"frequency",

"monetary_total",

"active_days",

"recent_30d_spend",

"prev_30d_spend",

"spend_trend",

]

# Fill missing values with 0.0 for the following columns

for col in fill_zero_cols:

model_base[col] = model_base[col].fillna(0.0)

# Fill missing values with a large value for the following columns

model_base["recency_days"] = model_base["recency_days"].fillna(observation_days + 1)

model_base["avg_order_value"] = model_base["avg_order_value"].fillna(0.0)

# last_purchase_date is not used as model feature directly

model_base = model_base.drop(columns=["last_purchase_date"], errors="ignore")

model_base.head()

[12]:

| customer_id | signup_date | country | customer_segment | acquisition_channel | frequency | monetary_total | active_days | avg_order_value | recency_days | recent_30d_spend | prev_30d_spend | spend_trend | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | C0001 | 2023-04-07 | CH | Standard | Referral | 3.0 | 112.71 | 3.0 | 37.570 | 25.0 | 54.76 | 0.0 | 54.76 |

| 1 | C0002 | 2024-08-19 | IT | Standard | Paid Ads | 0.0 | 0.00 | 0.0 | 0.000 | 181.0 | 0.00 | 0.0 | 0.00 |

| 2 | C0003 | 2024-05-24 | ES | Budget | Organic | 0.0 | 0.00 | 0.0 | 0.000 | 181.0 | 0.00 | 0.0 | 0.00 |

| 3 | C0004 | 2023-12-18 | IT | Standard | Referral | 2.0 | 48.47 | 2.0 | 24.235 | 99.0 | 0.00 | 0.0 | 0.00 |

| 4 | C0005 | 2023-12-14 | ES | Standard | Organic | 1.0 | 49.24 | 1.0 | 49.240 | 61.0 | 0.00 | 0.0 | 0.00 |

SECTION F — Add Tenure Feature¶

[13]:

model_base["tenure_days"] = (reference_date - model_base["signup_date"]).dt.days

model_base[["customer_id", "signup_date", "tenure_days"]].head()

model_base.head()

[13]:

| customer_id | signup_date | country | customer_segment | acquisition_channel | frequency | monetary_total | active_days | avg_order_value | recency_days | recent_30d_spend | prev_30d_spend | spend_trend | tenure_days | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | C0001 | 2023-04-07 | CH | Standard | Referral | 3.0 | 112.71 | 3.0 | 37.570 | 25.0 | 54.76 | 0.0 | 54.76 | 665 |

| 1 | C0002 | 2024-08-19 | IT | Standard | Paid Ads | 0.0 | 0.00 | 0.0 | 0.000 | 181.0 | 0.00 | 0.0 | 0.00 | 165 |

| 2 | C0003 | 2024-05-24 | ES | Budget | Organic | 0.0 | 0.00 | 0.0 | 0.000 | 181.0 | 0.00 | 0.0 | 0.00 | 252 |

| 3 | C0004 | 2023-12-18 | IT | Standard | Referral | 2.0 | 48.47 | 2.0 | 24.235 | 99.0 | 0.00 | 0.0 | 0.00 | 410 |

| 4 | C0005 | 2023-12-14 | ES | Standard | Organic | 1.0 | 49.24 | 1.0 | 49.240 | 61.0 | 0.00 | 0.0 | 0.00 | 414 |

SECTION G — Handle Categorical Features (One-Hot Encoding)¶

Categorical fields (country, customer_segment, acquisition_channel) cannot be used directly by most ML models. We one-hot encode them into binary indicator columns.

We avoid arbitrary ordinal encoding here because there is no meaningful numeric order between categories.

[14]:

# Identify the column types so far

model_base.dtypes

[14]:

customer_id str

signup_date datetime64[us]

country str

customer_segment str

acquisition_channel str

frequency float64

monetary_total float64

active_days float64

avg_order_value float64

recency_days float64

recent_30d_spend float64

prev_30d_spend float64

spend_trend float64

tenure_days int64

dtype: object

[15]:

# Select the categorical columns dedicatedly

categorical_cols = ["country", "customer_segment", "acquisition_channel"]

numeric_cols = [

"recency_days",

"frequency",

"monetary_total",

"avg_order_value",

"active_days",

"recent_30d_spend",

"prev_30d_spend",

"spend_trend",

"tenure_days",

]

# Keep a clean feature frame (exclude identifiers/date columns)

feature_input = model_base[["customer_id", "signup_date"] + categorical_cols + numeric_cols].copy()

feature_input.head()

[15]:

| customer_id | signup_date | country | customer_segment | acquisition_channel | recency_days | frequency | monetary_total | avg_order_value | active_days | recent_30d_spend | prev_30d_spend | spend_trend | tenure_days | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | C0001 | 2023-04-07 | CH | Standard | Referral | 25.0 | 3.0 | 112.71 | 37.570 | 3.0 | 54.76 | 0.0 | 54.76 | 665 |

| 1 | C0002 | 2024-08-19 | IT | Standard | Paid Ads | 181.0 | 0.0 | 0.00 | 0.000 | 0.0 | 0.00 | 0.0 | 0.00 | 165 |

| 2 | C0003 | 2024-05-24 | ES | Budget | Organic | 181.0 | 0.0 | 0.00 | 0.000 | 0.0 | 0.00 | 0.0 | 0.00 | 252 |

| 3 | C0004 | 2023-12-18 | IT | Standard | Referral | 99.0 | 2.0 | 48.47 | 24.235 | 2.0 | 0.00 | 0.0 | 0.00 | 410 |

| 4 | C0005 | 2023-12-14 | ES | Standard | Organic | 61.0 | 1.0 | 49.24 | 49.240 | 1.0 | 0.00 | 0.0 | 0.00 | 414 |

[16]:

# One-hot encode the categorical columns

preprocessor = ColumnTransformer(

transformers=[

("cat", OneHotEncoder(handle_unknown="ignore", sparse_output=False), categorical_cols),

("num", "passthrough", numeric_cols),

]

)

# Fit the preprocessor on the feature input

X_array = preprocessor.fit_transform(feature_input[categorical_cols + numeric_cols])

# Get the feature names from the preprocessor

cat_feature_names = preprocessor.named_transformers_["cat"].get_feature_names_out(categorical_cols).tolist()

final_feature_names = cat_feature_names + numeric_cols

# Create a DataFrame with the one-hot encoded features

X = pd.DataFrame(X_array, columns=final_feature_names, index=feature_input.index)

# Print the number of one-hot columns created and the total number of feature columns in X

print("One-hot columns created:", len(cat_feature_names))

print("Total feature columns in X:", X.shape[1])

X.head()

One-hot columns created: 12

Total feature columns in X: 21

[16]:

| country_CH | country_DE | country_ES | country_FR | country_IT | customer_segment_Budget | customer_segment_Premium | customer_segment_Standard | acquisition_channel_Affiliate | acquisition_channel_Organic | ... | acquisition_channel_Referral | recency_days | frequency | monetary_total | avg_order_value | active_days | recent_30d_spend | prev_30d_spend | spend_trend | tenure_days | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 0.0 | 0.0 | ... | 1.0 | 25.0 | 3.0 | 112.71 | 37.570 | 3.0 | 54.76 | 0.0 | 54.76 | 665.0 |

| 1 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 0.0 | 0.0 | 1.0 | 0.0 | 0.0 | ... | 0.0 | 181.0 | 0.0 | 0.00 | 0.000 | 0.0 | 0.00 | 0.0 | 0.00 | 165.0 |

| 2 | 0.0 | 0.0 | 1.0 | 0.0 | 0.0 | 1.0 | 0.0 | 0.0 | 0.0 | 1.0 | ... | 0.0 | 181.0 | 0.0 | 0.00 | 0.000 | 0.0 | 0.00 | 0.0 | 0.00 | 252.0 |

| 3 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 0.0 | 0.0 | 1.0 | 0.0 | 0.0 | ... | 1.0 | 99.0 | 2.0 | 48.47 | 24.235 | 2.0 | 0.00 | 0.0 | 0.00 | 410.0 |

| 4 | 0.0 | 0.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 0.0 | 1.0 | ... | 0.0 | 61.0 | 1.0 | 49.24 | 49.240 | 1.0 | 0.00 | 0.0 | 0.00 | 414.0 |

5 rows × 21 columns

SECTION H — Final Dataset Assembly¶

[17]:

# Join target y

final_dataset = pd.concat(

[

model_base[["customer_id"]].reset_index(drop=True),

X.reset_index(drop=True),

label_df[["future_revenue_90d"]].reset_index(drop=True),

],

axis=1,

)

final_dataset.head()

[17]:

| customer_id | country_CH | country_DE | country_ES | country_FR | country_IT | customer_segment_Budget | customer_segment_Premium | customer_segment_Standard | acquisition_channel_Affiliate | ... | recency_days | frequency | monetary_total | avg_order_value | active_days | recent_30d_spend | prev_30d_spend | spend_trend | tenure_days | future_revenue_90d | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | C0001 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 0.0 | ... | 25.0 | 3.0 | 112.71 | 37.570 | 3.0 | 54.76 | 0.0 | 54.76 | 665.0 | 0.00 |

| 1 | C0002 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 0.0 | 0.0 | 1.0 | 0.0 | ... | 181.0 | 0.0 | 0.00 | 0.000 | 0.0 | 0.00 | 0.0 | 0.00 | 165.0 | 0.00 |

| 2 | C0003 | 0.0 | 0.0 | 1.0 | 0.0 | 0.0 | 1.0 | 0.0 | 0.0 | 0.0 | ... | 181.0 | 0.0 | 0.00 | 0.000 | 0.0 | 0.00 | 0.0 | 0.00 | 252.0 | 32.47 |

| 3 | C0004 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 0.0 | 0.0 | 1.0 | 0.0 | ... | 99.0 | 2.0 | 48.47 | 24.235 | 2.0 | 0.00 | 0.0 | 0.00 | 410.0 | 48.28 |

| 4 | C0005 | 0.0 | 0.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 0.0 | ... | 61.0 | 1.0 | 49.24 | 49.240 | 1.0 | 0.00 | 0.0 | 0.00 | 414.0 | 63.55 |

5 rows × 23 columns

[18]:

print("Final dataset shape:", final_dataset.shape)

print("\nSample rows:")

display(final_dataset.head(5))

print("\nLeakage check (date ranges used):")

print(f"Observation window used for features: [{obs_start.date()}, {obs_end.date()}]")

print(f"Prediction window used for label: ({pred_start.date()}, {pred_end.date()}]")

print("No transactions after t are used in feature engineering.")

Final dataset shape: (1200, 23)

Sample rows:

| customer_id | country_CH | country_DE | country_ES | country_FR | country_IT | customer_segment_Budget | customer_segment_Premium | customer_segment_Standard | acquisition_channel_Affiliate | ... | recency_days | frequency | monetary_total | avg_order_value | active_days | recent_30d_spend | prev_30d_spend | spend_trend | tenure_days | future_revenue_90d | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | C0001 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 0.0 | ... | 25.0 | 3.0 | 112.71 | 37.570 | 3.0 | 54.76 | 0.0 | 54.76 | 665.0 | 0.00 |

| 1 | C0002 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 0.0 | 0.0 | 1.0 | 0.0 | ... | 181.0 | 0.0 | 0.00 | 0.000 | 0.0 | 0.00 | 0.0 | 0.00 | 165.0 | 0.00 |

| 2 | C0003 | 0.0 | 0.0 | 1.0 | 0.0 | 0.0 | 1.0 | 0.0 | 0.0 | 0.0 | ... | 181.0 | 0.0 | 0.00 | 0.000 | 0.0 | 0.00 | 0.0 | 0.00 | 252.0 | 32.47 |

| 3 | C0004 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 0.0 | 0.0 | 1.0 | 0.0 | ... | 99.0 | 2.0 | 48.47 | 24.235 | 2.0 | 0.00 | 0.0 | 0.00 | 410.0 | 48.28 |

| 4 | C0005 | 0.0 | 0.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 0.0 | ... | 61.0 | 1.0 | 49.24 | 49.240 | 1.0 | 0.00 | 0.0 | 0.00 | 414.0 | 63.55 |

5 rows × 23 columns

Leakage check (date ranges used):

Observation window used for features: [2024-08-04, 2025-01-31]

Prediction window used for label: (2025-01-31, 2025-05-01]

No transactions after t are used in feature engineering.

SECTION H2 — Pre-ML: Correlation, Redundancy, Scaling & Split¶

Before feeding the dataset to an ML model, we perform:

Pre-ML checks: missing values, duplicates, constant/near-constant columns in the final feature matrix.

Correlation analysis: heatmap and identification of highly correlated numeric features (and one-hot redundancy).

Redundancy handling: optionally drop one level per categorical (to avoid perfect multicollinearity) and drop numeric pairs above a correlation threshold.

Train/validation split: reproducible split for model development (for multiple reference dates in production, use a temporal split).

Scaling: fit scaler on training data only, then transform both train and validation to avoid leakage.

[19]:

# ---------------------------------------------------------------------------

# Pre-ML check: sanity on the final feature matrix (before split/scaling)

# ---------------------------------------------------------------------------

def pre_ml_checks(df, feature_columns, target_column="future_revenue_90d"):

"""

Run basic sanity checks on the dataset intended for ML.

Parameters

----------

df : pd.DataFrame

Full dataset including features and target.

feature_columns : list of str

Column names used as features (exclude IDs and target).

target_column : str

Name of the target column.

Returns

-------

dict

Summary of checks: missing, duplicates, constant columns.

"""

X = df[feature_columns]

out = {}

# Missing values

missing = X.isna().sum()

out["missing"] = missing[missing > 0]

if out["missing"].empty:

out["missing"] = "No missing values in features."

# Duplicate rows (in feature space)

out["n_duplicates"] = X.duplicated().sum()

# Constant or near-constant columns (zero variance)

constant = []

for col in X.columns:

if X[col].nunique() <= 1:

constant.append(col)

out["constant_columns"] = constant if constant else "None"

return out

# Feature columns = everything in final_dataset except ID and target

FEATURE_COLS = [c for c in final_dataset.columns

if c not in ("customer_id", "future_revenue_90d")]

TARGET_COL = "future_revenue_90d"

checks = pre_ml_checks(final_dataset, FEATURE_COLS, TARGET_COL)

print("Pre-ML checks (final feature matrix):")

print(" Missing per column:", checks["missing"])

print(" Duplicate rows (features):", checks["n_duplicates"])

print(" Constant/near-constant columns:", checks["constant_columns"])

Pre-ML checks (final feature matrix):

Missing per column: No missing values in features.

Duplicate rows (features): 2

Constant/near-constant columns: None

[20]:

# ---------------------------------------------------------------------------

# Correlation analysis: numeric features only (one-hot dummies are 0/1)

# ---------------------------------------------------------------------------

import matplotlib.pyplot as plt

import seaborn as sns

# Numeric feature columns (same as used in encoding)

NUMERIC_FOR_CORR = [

"recency_days", "frequency", "monetary_total", "avg_order_value",

"active_days", "recent_30d_spend", "prev_30d_spend", "spend_trend", "tenure_days",

]

X_numeric = final_dataset[NUMERIC_FOR_CORR]

corr_matrix = X_numeric.corr()

fig, ax = plt.subplots(figsize=(10, 8))

sns.heatmap(corr_matrix, annot=True, fmt=".2f", cmap="RdBu_r", center=0,

square=True, linewidths=0.5, ax=ax)

ax.set_title("Correlation matrix (numeric features)")

plt.tight_layout()

plt.show()

# Pairs with |correlation| above threshold (e.g. 0.9 or 0.95)

CORR_THRESHOLD = 0.9

high_corr_pairs = []

for i in range(len(corr_matrix.columns)):

for j in range(i + 1, len(corr_matrix.columns)):

if abs(corr_matrix.iloc[i, j]) >= CORR_THRESHOLD:

high_corr_pairs.append(

(corr_matrix.columns[i], corr_matrix.columns[j], corr_matrix.iloc[i, j])

)

print(f"\nNumeric pairs with |correlation| >= {CORR_THRESHOLD}:")

if high_corr_pairs:

for a, b, r in high_corr_pairs:

print(f" {a} <-> {b}: {r:.3f}")

else:

print(" None.")

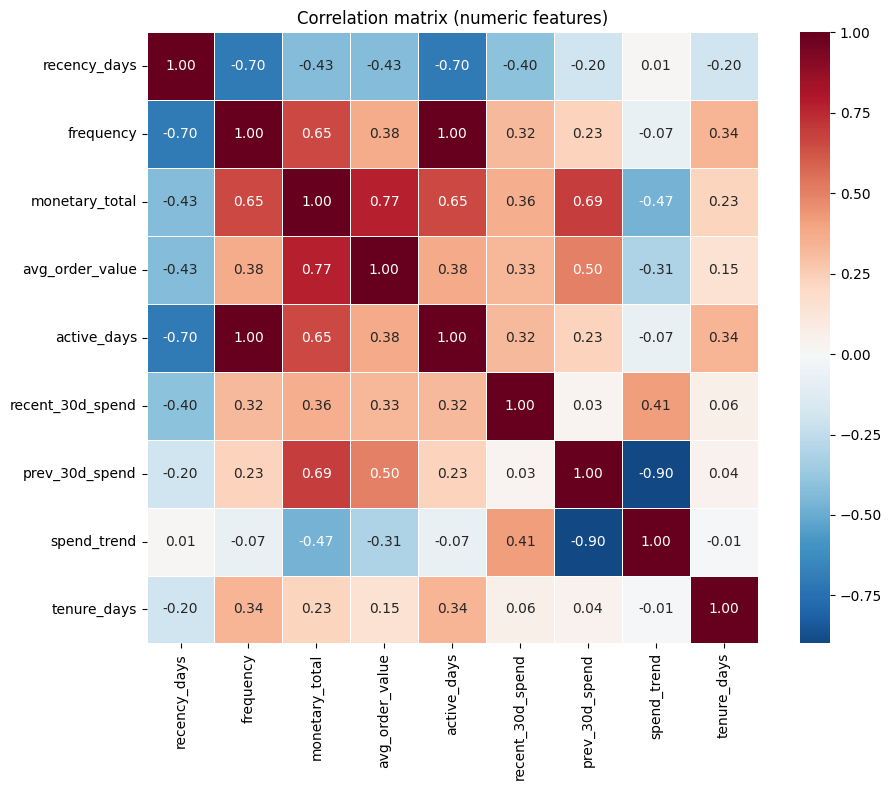

Numeric pairs with |correlation| >= 0.9:

frequency <-> active_days: 0.998

Interpreting correlation and what to do about it¶

Which features tend to correlate?

Numeric behavioural features often move together: e.g.

frequencyandactive_days(both count activity in the observation window), ormonetary_totalwithrecent_30d_spend(total spend vs a component of it).avg_order_valueis derived asmonetary_total / frequency, so it is algebraically tied to those two. In this dataset we may see strong correlations among these.One-hot encoded categoricals are perfectly redundant within each group: the columns for one categorical (e.g. all

country_*) sum to 1 for every row, so one column is a linear combination of the others.

What can we do?

One-hot: Drop one level per categorical (e.g. the first alphabetically). We keep the rest; the dropped level becomes the „reference“ in linear models. This removes perfect multicollinearity within each categorical.

Numeric pairs: For pairs with |correlation| above a chosen threshold (e.g. 0.9 or 0.95), we can drop one of the two. Which one to drop is a modelling choice (e.g. keep the one that is easier to interpret or more stable).

Why do it?

Linear / penalized linear models: High or perfect correlation makes coefficient estimates unstable (large variance) and can break solvers. Dropping redundant columns stabilizes estimates and keeps the model well-defined.

Interpretability: Fewer redundant features make coefficients easier to interpret (e.g. „effect of country X vs reference“ instead of an ill-defined mix).

Tree-based models (Random Forest, XGBoost, etc.) are less sensitive to multicollinearity; they can still benefit from fewer noisy/redundant features but do not require this step for numerical stability.

How we implement it below

For categoricals: we identify one column to drop per group (e.g. first per group) and exclude them from the feature set.

For numerics: we compute the correlation matrix, find pairs above a threshold (e.g. 0.95), and drop one column from each pair (e.g. the second in a fixed order) so that no remaining pair exceeds the threshold. The next cell implements both steps.

[21]:

# ---------------------------------------------------------------------------

# Redundancy: one-hot "drop first" and optional removal of highly correlated numerics

# ---------------------------------------------------------------------------

# (1) One-hot encoding created one column per level; for linear models we often

# drop one level per categorical to avoid perfect multicollinearity.

# Here we define which columns to drop (one per categorical group).

CATEGORICAL_GROUPS = {

"country": [c for c in FEATURE_COLS if c.startswith("country_")],

"customer_segment": [c for c in FEATURE_COLS if c.startswith("customer_segment_")],

"acquisition_channel": [c for c in FEATURE_COLS if c.startswith("acquisition_channel_")],

}

# Drop the first alphabetically (e.g. country_CH, customer_segment_Budget, acquisition_channel_Affiliate)

COLS_TO_DROP_ONEHOT = [cols[0] for cols in CATEGORICAL_GROUPS.values()]

print("One-hot columns dropped (one per group) to avoid multicollinearity:", COLS_TO_DROP_ONEHOT)

# (2) Optionally drop one of each highly correlated numeric pair (keep first, drop second)

def get_columns_to_drop_high_corr(corr_matrix, threshold=0.95):

"""Return a set of column names to drop so that no pair has |corr| >= threshold."""

to_drop = set()

for i in range(len(corr_matrix.columns)):

for j in range(i + 1, len(corr_matrix.columns)):

if abs(corr_matrix.iloc[i, j]) >= threshold:

# Drop the second column (j)

to_drop.add(corr_matrix.columns[j])

return to_drop

HIGH_CORR_DROP_THRESHOLD = 0.95

cols_drop_high_corr = get_columns_to_drop_high_corr(corr_matrix, HIGH_CORR_DROP_THRESHOLD)

print(f"\nNumeric columns to drop (|corr| >= {HIGH_CORR_DROP_THRESHOLD}):", cols_drop_high_corr or "None")

# Build the reduced feature list (optional: apply both one-hot drop and high-corr drop)

FEATURE_COLS_REDUCED = [

c for c in FEATURE_COLS

if c not in COLS_TO_DROP_ONEHOT and c not in cols_drop_high_corr

]

print(f"\nFeature count: original = {len(FEATURE_COLS)}, reduced = {len(FEATURE_COLS_REDUCED)}")

One-hot columns dropped (one per group) to avoid multicollinearity: ['country_CH', 'customer_segment_Budget', 'acquisition_channel_Affiliate']

Numeric columns to drop (|corr| >= 0.95): {'active_days'}

Feature count: original = 21, reduced = 17

[22]:

data_final = final_dataset[FEATURE_COLS_REDUCED+[TARGET_COL]]

print(data_final.info())

data_final.head()

<class 'pandas.DataFrame'>

RangeIndex: 1200 entries, 0 to 1199

Data columns (total 18 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 country_DE 1200 non-null float64

1 country_ES 1200 non-null float64

2 country_FR 1200 non-null float64

3 country_IT 1200 non-null float64

4 customer_segment_Premium 1200 non-null float64

5 customer_segment_Standard 1200 non-null float64

6 acquisition_channel_Organic 1200 non-null float64

7 acquisition_channel_Paid Ads 1200 non-null float64

8 acquisition_channel_Referral 1200 non-null float64

9 recency_days 1200 non-null float64

10 frequency 1200 non-null float64

11 monetary_total 1200 non-null float64

12 avg_order_value 1200 non-null float64

13 recent_30d_spend 1200 non-null float64

14 prev_30d_spend 1200 non-null float64

15 spend_trend 1200 non-null float64

16 tenure_days 1200 non-null float64

17 future_revenue_90d 1200 non-null float64

dtypes: float64(18)

memory usage: 168.9 KB

None

[22]:

| country_DE | country_ES | country_FR | country_IT | customer_segment_Premium | customer_segment_Standard | acquisition_channel_Organic | acquisition_channel_Paid Ads | acquisition_channel_Referral | recency_days | frequency | monetary_total | avg_order_value | recent_30d_spend | prev_30d_spend | spend_trend | tenure_days | future_revenue_90d | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 0.0 | 0.0 | 1.0 | 25.0 | 3.0 | 112.71 | 37.570 | 54.76 | 0.0 | 54.76 | 665.0 | 0.00 |

| 1 | 0.0 | 0.0 | 0.0 | 1.0 | 0.0 | 1.0 | 0.0 | 1.0 | 0.0 | 181.0 | 0.0 | 0.00 | 0.000 | 0.00 | 0.0 | 0.00 | 165.0 | 0.00 |

| 2 | 0.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 0.0 | 0.0 | 181.0 | 0.0 | 0.00 | 0.000 | 0.00 | 0.0 | 0.00 | 252.0 | 32.47 |

| 3 | 0.0 | 0.0 | 0.0 | 1.0 | 0.0 | 1.0 | 0.0 | 0.0 | 1.0 | 99.0 | 2.0 | 48.47 | 24.235 | 0.00 | 0.0 | 0.00 | 410.0 | 48.28 |

| 4 | 0.0 | 1.0 | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 0.0 | 0.0 | 61.0 | 1.0 | 49.24 | 49.240 | 0.00 | 0.0 | 0.00 | 414.0 | 63.55 |

[23]:

# save the final dataset to a CSV file

data_final.to_csv("data/final_dataset.csv", sep=";", index=False)

We have finished (showcasing) feature engineering, but still need to normalize (as an example of preprocessing steps) the data before we can feed it to train the model.¶

Why we still need preprocessing

Many models are sensitive to feature scale (e.g., linear models with regularization, kNN, neural nets). Without scaling, large-magnitude features (e.g.

monetary_total,tenure_days) can dominate the objective and distort learning.Some preprocessing steps are required for numerical stability and interpretability (e.g., removing perfect multicollinearity from one-hot encoded categoricals).

When to do preprocessing?

Normalization (and similar preprocessing) must be fitted after the train/validation split.

Even though we have saved final_dataset.csv, the data is not yet in the form we should feed directly into many ML algorithms.

Why we split first, then fit preprocessing on train only (leakage avoidance)

Preprocessing often computes statistics from the data (mean/std for scaling, quantiles for clipping, PCA directions, feature selection thresholds, imputation values, etc.). If those statistics are computed using all rows (train + validation), information from the validation set leaks into training.

Correct pattern:

Split into train/validation.

Fit preprocessing steps using training data only.

Apply (“transform”) the fitted preprocessing to train and validation.

What goes wrong if we fit preprocessing before the split:

The model indirectly “sees” validation distribution information via the preprocessing statistics.

Validation metrics become optimistically biased and won’t reflect true generalization.

Note: the correlation-based feature dropping shown above is also a form of feature selection. In a strict pipeline, it should be decided using training data only. For this teaching notebook we compute it once for simplicity, but the same leakage principle applies.

[24]:

# ---------------------------------------------------------------------------

# Train/validation split (reproducible; for production with multiple reference dates, use temporal split)

# ---------------------------------------------------------------------------

from sklearn.model_selection import train_test_split

SPLIT_SEED = SEED # use same as notebook

VAL_SIZE = 0.2

# Use reduced feature set if we applied redundancy handling; else use full feature list

X_ml = final_dataset[FEATURE_COLS_REDUCED]

y_ml = final_dataset[TARGET_COL]

X_train, X_val, y_train, y_val = train_test_split(

X_ml, y_ml, test_size=VAL_SIZE, random_state=SPLIT_SEED, shuffle=True

)

print(f"Train size: {len(X_train)}, Validation size: {len(X_val)}")

print(f"Train target mean: {y_train.mean():.2f}, val target mean: {y_val.mean():.2f}")

Train size: 960, Validation size: 240

Train target mean: 47.12, val target mean: 43.65

As mentioned, after **splitting* into train/validation, we can now

Fit preprocessing steps using training data only.

Apply (“transform”) the fitted preprocessing to train and validation.

Separating training and validation data for fitting and applying helps avoid:

that the model indirectly “sees” validation distribution information via the preprocessing statistics.

validation metrics become optimistically biased and won’t reflect true generalization.

[25]:

# ---------------------------------------------------------------------------

# Scaling: fit on training data only, then transform train and validation

# ---------------------------------------------------------------------------

from sklearn.preprocessing import StandardScaler

scaler = StandardScaler()

X_train_scaled = scaler.fit_transform(X_train)

X_val_scaled = scaler.transform(X_val)

# Optional: wrap back into DataFrames for readability

X_train_scaled_df = pd.DataFrame(X_train_scaled, columns=FEATURE_COLS_REDUCED, index=X_train.index)

X_val_scaled_df = pd.DataFrame(X_val_scaled, columns=FEATURE_COLS_REDUCED, index=X_val.index)

print("Scaled feature matrices ready for ML.")

print("X_train_scaled shape:", X_train_scaled.shape)

print("X_val_scaled shape:", X_val_scaled.shape)

Scaled feature matrices ready for ML.

X_train_scaled shape: (960, 17)

X_val_scaled shape: (240, 17)

[26]:

# ---------------------------------------------------------------------------

# Export train/validation splits (raw + scaled) for downstream modeling

# ---------------------------------------------------------------------------

from pathlib import Path

PROJECT_ROOT = Path.cwd()

PROJECT_ROOT = Path.cwd()

if not (PROJECT_ROOT / "data").is_dir():

PROJECT_ROOT = PROJECT_ROOT.parent

DATA_DIR = PROJECT_ROOT / "data"

DATA_DIR.mkdir(parents=True, exist_ok=True)

# Raw splits

X_train.to_csv(DATA_DIR / "X_train.csv", index=False)

X_val.to_csv(DATA_DIR / "X_val.csv", index=False)

y_train.to_csv(DATA_DIR / "y_train.csv", index=False, header=[TARGET_COL])

y_val.to_csv(DATA_DIR / "y_val.csv", index=False, header=[TARGET_COL])

# Scaled splits

X_train_scaled_df.to_csv(DATA_DIR / "X_train_scaled.csv", index=False)

X_val_scaled_df.to_csv(DATA_DIR / "X_val_scaled.csv", index=False)

# Save metadata to help the modeling notebook/script load consistently

(pd.Series(FEATURE_COLS_REDUCED, name="feature_name")

.to_csv(DATA_DIR / "feature_columns.csv", index=False))

# Optional: persist the fitted scaler so the exact same transform can be reused

# Detailed explanation see markdown below

try:

import joblib

joblib.dump(scaler, DATA_DIR / "standard_scaler.joblib")

print("Saved scaler to:", DATA_DIR / "standard_scaler.joblib")

except Exception as e:

print("Could not save scaler (joblib not available or write error):", repr(e))

print("Saved train/val splits to:", DATA_DIR.resolve())

print("Files written:")

for name in [

"X_train.csv", "X_val.csv", "y_train.csv", "y_val.csv",

"X_train_scaled.csv", "X_val_scaled.csv",

"feature_columns.csv",

]:

print(" -", name)

Saved scaler to: /Users/veit/cusy/trn/ai-tutorial/docs/1intro/data/standard_scaler.joblib

Saved train/val splits to: /Users/veit/cusy/trn/ai-tutorial/docs/1intro/data

Files written:

- X_train.csv

- X_val.csv

- y_train.csv

- y_val.csv

- X_train_scaled.csv

- X_val_scaled.csv

- feature_columns.csv

Why did we save standard_scaler.joblib?¶

In addition to writing the CSV splits (raw and scaled), we also persist the fitted scaler object as data/standard_scaler.joblib.

Why store the scaler?

The scaler contains the exact means and standard deviations that were learned from the training data.

Any future code (another notebook, a serving script, a retraining job) that wants to use this model should apply exactly the same scaling to new data, otherwise the model will see a different feature distribution and behave unpredictably.

Storing the scaler is a common production pattern: you ship both the model and its preprocessing steps.

How to use it later (pseudo-code)

===pseudo-code start===

import joblib

import pandas as pd

# 1. Load the scaler that was fitted in this notebook

scaler = joblib.load("../data/standard_scaler.joblib")

# 2. Load or build new feature matrix with the *same columns* as during training

X_new = pd.read_csv("../data/new_raw_features.csv") # or any DataFrame

X_new = X_new[FEATURE_COLS_REDUCED] # enforce same column order

# 3. Apply the exact same scaling

X_new_scaled = scaler.transform(X_new)

# 4. Feed X_new_scaled into the trained model for predictions

# y_pred = trained_model.predict(X_new_scaled)

===pseudo-code end===

In this course, notebooks/02_async_session.ipynb reads the pre-scaled CSVs directly and does not need the .joblib file.

Thus, the scaler file is there to illustrate how you would structure a realistic pipeline where preprocessing is reused consistently across training, evaluation, deployment, and monitoring.

SECTION I — Optional Sanity Plot¶

[27]:

import matplotlib.pyplot as plt

fig, axes = plt.subplots(1, 2, figsize=(12, 4))

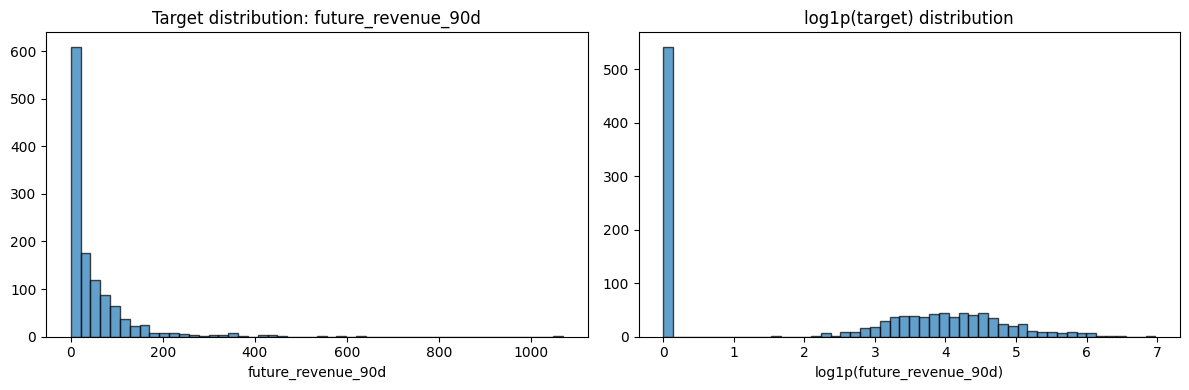

axes[0].hist(final_dataset["future_revenue_90d"], bins=50, edgecolor="black", alpha=0.7)

axes[0].set_title("Target distribution: future_revenue_90d")

axes[0].set_xlabel("future_revenue_90d")

axes[1].hist(np.log1p(final_dataset["future_revenue_90d"]), bins=50, edgecolor="black", alpha=0.7)

axes[1].set_title("log1p(target) distribution")

axes[1].set_xlabel("log1p(future_revenue_90d)")

plt.tight_layout()

plt.show()

print("Target is right-skewed (common for revenue). log1p transform can be considered in downstream modeling.")

Target is right-skewed (common for revenue). log1p transform can be considered in downstream modeling.